B2B telecommunication companies (telcos) find themselves in a transformative landscape of technology orchestration and platform evolution — leading to the potential for redefining their business models. Our in-depth report, “The Future Of B2B Telco”, navigates the intricate journey of telcos transitioning into tech orchestrators, seamlessly integrating connectivity, cloud solutions, cybersecurity, data, and applications.

In an era marked by the commoditization of traditional connectivity, telcos face a pivotal crossroads. The decline of fixed voice, not offset by data connectivity, coupled with the ascendancy of hyperscalers and digital/tech players, propels telcos toward a rapid business model shift. The challenge lies in avoiding strategic deadlocks and articulating a precise strategy to maintain their unique position in the market.

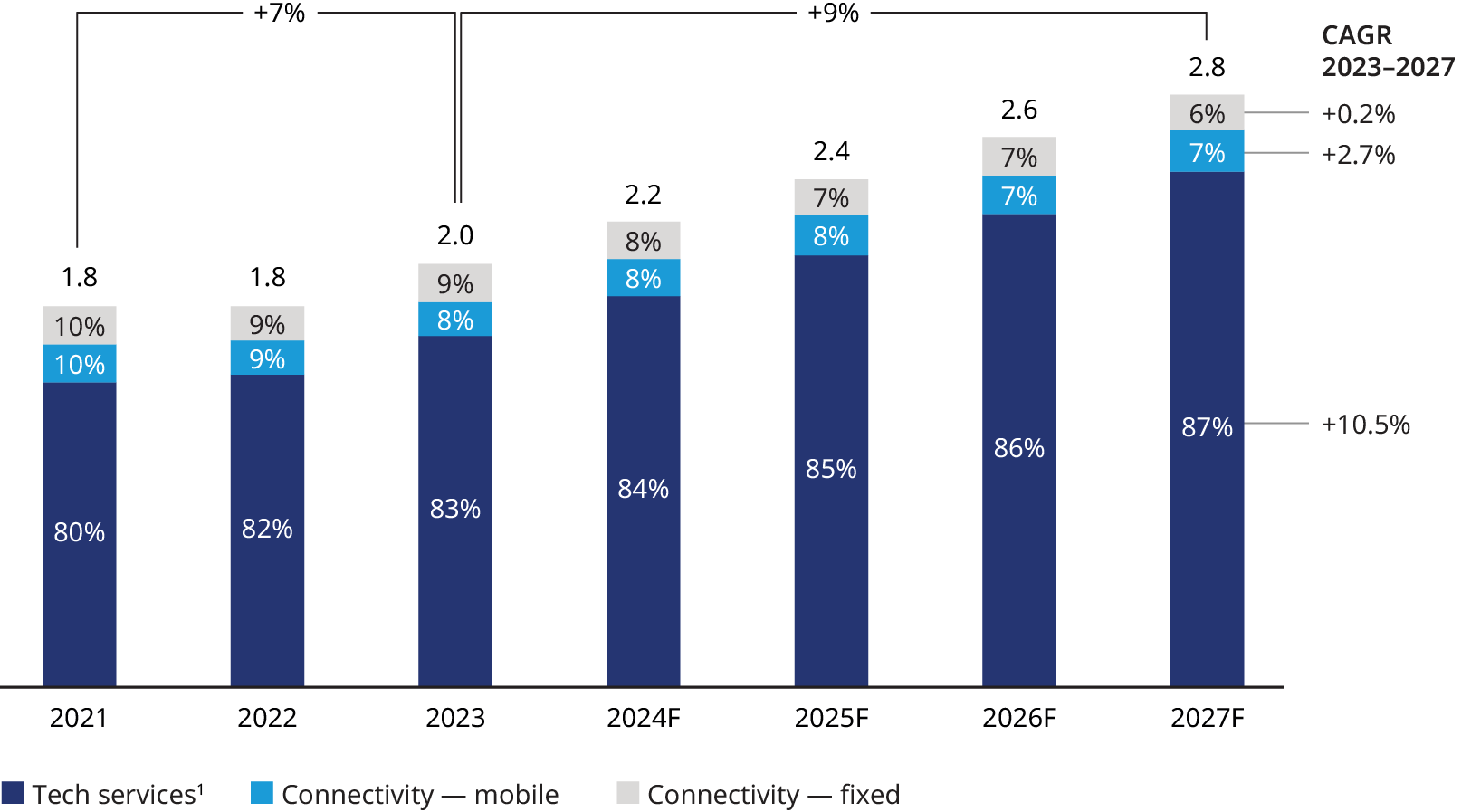

The rise of tech services in B2B Telcos

The commoditization of traditional telecom connectivity is rapidly increasing, resulting in a decline in fixed voice revenue ranging from 8% to 15% annually, depending on the location. This decline is not being offset by the growth in data and mobile connectivity revenues, which are only growing by 1% to 3% per year. However, there is good news in the form of the thriving tech services market, which is growing at a rate of approximately 10.5% per year.

In 2021, tech services accounted for 80% of the B2B technology and connectivity market, and over the past three years, their market share has increased by 3 percentage points to reach 83%. It is expected that by 2027, tech services will gain an additional 4 percentage points, reaching an 87% market share. This promising market opportunity has prompted most telco B2B organizations to focus on and expand their tech services business in recent years.

However, the mix of tech services varies greatly among operators at different stages of their B2B journey. Some operators have already surpassed the 50% mark, while others are at or below 25%. The challenge for operators is not only to capture part of this growth but also to manage the transition from a high margin, low growth business to a low margin, high growth business.

Strategic focus areas shaping the integration landscape

Our report guides you through five pivotal technology areas shaping the integration landscape. Telcos, leveraging their distinctive strengths, emerge as pioneers in these critical technological frontiers:

- Cybersecurity: Telcos carve a niche with network security, identity and access management , endpoint security, zero trust, and security operation centers (SOC). The cybersecurity market share of telcos indicates untapped potential for growth.

- Cloud solutions: Telcos play a crucial role in private cloud services, reshaping connectivity architecture, and providing cloud orchestration and managed services.

- Data organization: Leveraging their access to abundant data, telcos secure critical infrastructure, pioneer sovereign cloud solutions, and delve into identity management.

- Edge computing: A natural fit for telcos, though a long-term bet, offering services for real-time processing in applications like industrial automation and smart cities.

- Internet of things (IoT) solutions: Despite being in its infancy, telcos assert a clear right to win in IoT solutions, focusing on selected vertical bets and navigating the convergence of IT and engineering.

Key trends and strategies crucial for the future success of B2B telecos

The importance of seamless integration

The report delves into the industrial applications race where telcos, IT services players, and hyperscalers vie for a position, but there is room for partnerships. The capability to orchestrate solutions by seamlessly integrating networks, cloud, data, applications, and security becomes paramount for the digitalization of the economy.

Shifting the paradigm to become platforms

As telcos evolve into platforms and industrial integrators, a radical portfolio simplification becomes imperative. Complexity gives way to strategic focus, amplifying agility and refining the organizational core. We explore inspiring examples of players cutting their portfolio while improving business agility and commercials.

Revolutionizing the go-to-market

The report further explores how telcos should embrace a paradigm shift from telco-first to tech-first in the go-to-market model. Seamless synchronization between sales and delivery, consultative selling, stronger margin visibility, new pricing models, and reimagined strategic partnerships are critical dimensions. This evolution ensures a cohesive approach between sales and delivery, a deep understanding of client needs, economic discipline in pricing, and dynamic collaborations. Simultaneously, a customer-centric focus unfolds, emphasizing an enterprise-first strategy while addressing the unique challenges and opportunities within the SME segment. This strategic realignment not only reshapes service delivery but also ensures a tailored and responsive approach to diverse client needs.

The skills challenge in telcos

The workforce challenge looms large as telcos adapt to new capabilities required for IT services. In our report, we look at the actions needed to lay the foundations for the future workforce requirements in telco B2B.

Integrating global innovation and local precision

In the dynamic B2B telco landscape, the challenge lies in seamlessly integrating global innovation with local precision. Current organizational models face inefficiencies, restricting operating margins, agility, and customer experiences. To counter this, operators must adopt a transformative approach, establishing a unified global product function while maintaining local delivery and pre-sales focus. Shifting to a customer-centric model, simplification of structures, and strategic near and offshore initiatives become imperative, positioning B2B Telco for success in an evolving tech-centric future.

Unlocking value through tech unit carve-outs

Examining the triumphs of pioneers, the benefits of investing in and adapting organizational structures for non-connectivity pursuits in B2B telco are evident. Over the past five years, a trend of tech unit carve-outs has surged, often driven by shareholder pressure for value optimization. Initial assessments, comparing telco EV/REV multiples to pure-tech companies, suggest promising returns. However, unlocking value through a carve-out demands strategic rationales, granting the new unit autonomy in management, investments, channels, geography, and partnerships.

The process, while promising, poses challenges. Additionally, carving-out high-growth tech units raises concerns about the future of the remaining connectivity segment. Assessing whether the benefits outweigh the risks is operator and market-dependent, necessitating careful evaluation by management and investors. Solely financial motives for carve-outs may not justify the complexities, risking the re-allocation of value within the group rather than unleashing its full potential.